California Targets Wildfire Insurance Secrecy

Thanks in part to its climate and vegetation, wildfires have always been a part of life in California.

But in recent years, the severity of devastating wildfires has increased and the negative impacts are felt more widely by residents, businesses, federal, state, and local governments.

A study by the University of California, Irvine found that between the 1980s and the 2010s, the average wildfire severity increased by approximately 30%.

The 2018 wildfire season alone resulted in approximately $150 billion in total damages (including healthcare and indirect economic losses), roughly 0.7% of the entire US GDP for that year.

Insurance claims from wildfires have risen dramatically and so have residential wildfire insurance rates.

The insurance industry saw its profits wiped out by the 2017 and 2018 fire seasons, which resulted in more than $20 billion in insured losses back-to-back, a level of loss the market had not priced in.

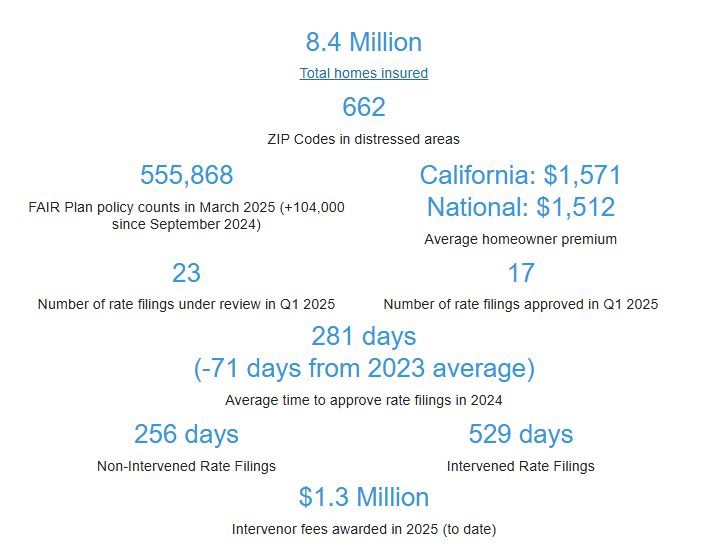

Insurers have paid out billions in claims for recent fires, leading to a "solvency crisis" where payouts exceed the premiums collected in the state for many years.

Several of America's biggest insurers now refuse to offer wildfire coverage to CA residents in high-risk areas.

In 2023, State Farm and Allstate stopped accepting new home insurance applications in California.

Even if you have or can get insurance, rates have skyrocketed.

In March, 2024 State Farm announced it would not renew 30,000 homeowner policies.

It also declined to continue offering commercial apartment building policies and said it won't renew the 42,000 it covered at the time.

With many people frozen out by commercial insurers, they have no choice but to turn to the last resort to cover their homes.

What Is California FAIR Plan Insurance?

The California FAIR Plan provides a last resort insurance option for homes and businesses that can't obtain private insurance.

Established by CA state legislators in 1968, FAIR (Fair Access to Insurance Requirements) was enacted to give individuals and companies unable to find private carriers to cover their property access to insurance, primarily for fire policies.

FAIR does cover "named perils" other than fire, but it's far from a comprehensive homeowners insurance policy.

FAIR Plan Insurance in California: What Does It Cover?

Insured Event | Standard FAIR Policy Coverage | Optional FAIR Policy Coverage | FAIR Policy Exclusions |

Fire | ✅ |

|

|

Lightning | ✅ |

|

|

Internal Explosion | ✅ |

|

|

Smoke | ✅ |

|

|

Windstorm & Hail | ❌ | ✅ |

|

Explosion | ❌ | ✅ |

|

Riot or Civil Commotion | ❌ | ✅ |

|

Aircraft & Vehicles | ❌ | ✅ |

|

Vandalism | ❌ | ✅ |

|

Volcanic Eruption | ❌ | ✅ |

|

Liability | ❌ | ❌ | ✅ |

Theft/Burglary | ❌ | ❌ | ✅ |

Water Damage | ❌ | ❌ | ✅ |

Medical Payments | ❌ | ❌ | ✅ |

Earthquakes* | ❌ | ❌ | ✅ |

*Earthquake insurance in CA is typically handled by the California Earthquake Authority (CEA).

Because FAIR coverage is so limited, homeowners who cannot receive a comprehensive policy from a private insurer are forced to purchase a Difference in Conditions (DIC) policy.

DIC policies are provided by private insurers in California.

Is California's FAIR Insurance a Good Deal for Homeowners?

The short answer? No.

Unlike car insurance, which is required by CA law, homeowners insurance is voluntary IF the property is 100% owned free and clear.

However, homeowners insurance is required by mortgage lenders in CA.

When a traditional bank, independent mortgage bank (IMB), credit union, or mortgage broker lends you money to finance a home, the primary collateral is the property itself.

All licensed lenders require homeowners insurance as a prerequisite for financing the purchase of residential property.

Since homeowners insurance isn't optional for most Californians (due to mortgages), and private insurers are rejecting applications in wildfire zones, the FAIR Plan becomes the only option left to close the deal.

A July 2025 SF Chronicle article revealed how much the FAIR Plan costs homeowners in every CA zip code.

Their analysis found that the statewide average for a standard homeowner's policy is roughly $1,400 per year.

In the most extreme cases found in the data, such as high-risk neighborhoods in San Jose, the average FAIR Plan premium reached over $21,000 per year — 15x or 1400% above the statewide average for a private policy.

What makes that number even more shocking is that it's for FAIR coverage alone.

A separate DIC policy typically costs between $1,500 to $3,000+ per year, depending on the value and location of the home.

The actual annual cost to fully cover a home in the high-risk zip code the Chronicle studied averages out to about $23,000 to $25,000 a year as opposed to $1,400 for homeowners insurance in other parts of the state.

Senate Bill 429: Cracking Open the "Black Box" of Insurance Algorithms

On October 10, 2025, Governor Gavin Newsom signed Senate Bill 429 into law.

Written and sponsored by state Sen. Dave Cortese as part of a "wildfire resilience package," Senate Bill 429 aims to make the decision-making process that private insurers use to raise premiums and refuse coverage in many areas of the state less of a "black box" and more transparent to the public.

According to the San Jose Spotlight:

"SB 429 addresses the rise in insurance premiums related to wildfires and, in many cases, insurance companies refusing to issue policies in California altogether. Cortese said insurance companies’ risk modeling is often kept secret, so the bill creates a wildfire safety and risk management program to develop a state wildfire catastrophe model. The bill calls for this program to be budgeted beginning Sept. 1, 2026."

Cortese's proposal is the first of its kind in the US to become law.

By creating a transparent, publicly accessible "public wildfire catastrophe model… the law will give consumers the ability to push back on secret wildfire risk algorithms insurance companies use to raise rates in California."

(Source: California Department of Insurance)

The Sustainable Insurance Strategy: A "Grand Bargain?"

The Sustainable Insurance Strategy was first announced by California Insurance Commissioner Ricardo Lara on September 21, 2023.

It coincided with Governor Newsom signing an Executive Order the same day directing immediate action to stabilize CA's insurance market.

The LA Times called the Strategy:

"A set of comprehensive regulations intended to stabilize rates and make it more attractive for insurers to write homeowners policies, especially in wildfire areas such as hillsides and canyons," characterizing it as a "grand bargain with the insurance industry to make the market more attractive."

The "grand bargain" will finally permit private insurers to use forward-looking Catastrophe Models to set rates in exchange for the companies' commitment to writing policies in wildfire-distressed areas, eventually aiming to cover at least 85% of their statewide market share in these distressed areas.

Senate Bill 429 gives the agreement teeth by mandating the creation of a transparent public Catastrophe Model that the regulator can use to approve or reject proposed rate hikes by private insurers that they justify using their proprietary "black box" pricing algorithms.

The Sustainable Insurance Strategy gives insurers permission to use AI-powered predictive modeling tools to set rates and Senate Bill 429 helps ensure private insurers can't abuse the system by mandating a transparent, public benchmark to keep prices honest.

Will this "grand bargain" make wildfire insurance more accessible, affordable, and transparent to California homeowners?

Only time will tell, but hopefully it's a big step in the right direction.

Resources Cited

Associated Press. "State Farm Stops Accepting New Home Insurance Applications in California." AP News, May 27, 2023.

Bay Area Council Economic Institute. "The Economic Impact of the 2018 California

Wildfires." Bay Area Council Economic Institute, n.d.

California Department of Forestry and Fire Protection (CAL FIRE). "Statistics." State of California, 2024.

California Department of Insurance. "Sustainable Insurance Strategy." State of California, 2024.

California FAIR Plan Association. "About the FAIR Plan." California FAIR Plan Association, n.d.

CBS News. "Allstate Stops Selling New Home Insurance Policies in California." CBS News, June 5, 2023.

Insurance Information Institute. "Facts + Statistics: Wildfires." Insurance Information Institute, 2024.

San Francisco Chronicle. "California Home Insurance Rates to Spike." San Francisco Chronicle, 2024.

University of California, Irvine. "UCI-Led Team Publishes First In-Depth Global Analysis of Wildfire Trends." UCI News, 2019.

Vives, Ruben. “State Farm Won’t Renew 72,000 Insurance Policies in California.” Los Angeles Times, March 23, 2024.

California Department of Insurance: "Commissioner Lara Announces Sustainable Insurance Strategy"

Balber, Carmen. “California to Create First Public Wildfire Catastrophe Model to Empower Homeowners with Insurance Wildfire ...” Consumer Watchdog, October 13, 2025.

For press requests or interview opportunities, reach out to our media team

media.na@ecoflow.com